From This Little-Known Pension Rule May Slash Your Social Security Benefit

If you are covered by a public sector pension, you may not get the Social Security payout you’re expecting.

Some U.S. workers who have paid into the Social Security system are in for a rude awakening when the checks start coming: Their benefits could be chopped up to $413 per month.

That is the maximum potential cut for 2015 stemming from the Windfall Elimination Provision (WEP), a little-understood rule that was signed into law in 1983 to prevent double-dipping from both Social Security and public sector pensions. A sister rule called the Government Pension Offset (GPO) can result in even sharper cuts to spousal and survivor benefits.

WEP affected about 1.5 million Social Security beneficiaries in 2012, and another 568,000 were hit by the GPO, according to the U.S. Social Security Administration (SSA). Most of those affected are teachers and employees of state and local government.

These two safeguards often come as big news to retirees. Until 2005, no law required that affected employees be informed by their employers. Even now, the law only requires employers to inform new workers of the possible impact on Social Security benefits earned in other jobs.

The Social Security Administration’s statement of benefits has included a generic description of the possible impact of WEP and GPO since 2007; for workers who are affected, the statement includes a link is included to an online tool where the impact on the individual can be calculated. People who have worked only in jobs not covered by Social Security get a letter indicating that they are not eligible.

Many retirees perceive the two rules as grossly unfair. Opponents have been pushing for repeal, so far to no effect.

Why WEP?

To understand the issue, you need to understand how Social Security benefits are distributed across the wealth spectrum of wage-earners.

The program uses a progressive formula that aims to return the highest amount to the lowest-earning workers—the same idea that drives our system of income tax brackets.

It is a complex formula, but here is the upshot: Without the WEP, a worker who had just 20 years of employment covered by Social Security, rather than 30, would be in position to get a much higher return because of those brackets.

Where is the double dip? The years in a job covered by a pension instead of Social Security.

“If you had worked in non-covered employment for a significant portion of your career, there should be a shared burden between the pension you receive from that period of your employment and from Social Security in providing your benefit,” says SSA Chief Actuary Stephen C. Goss. “Just because a person worked only a portion of their career with Social Security-covered employment, they should not be benefiting by getting a higher rate of return.”

If you are already receiving a qualifying pension when you file for Social Security, then the WEP formula kicks in immediately. The SSA asks a question about non-covered pensions when you file for benefits, and it also has access to the Internal Revenue Service Form 1099-R, which shows income from pensions and other retirement income.

If your pension payments start after you file, the adjustment will occur then.

If you have 30 years of Social Security-covered employment, no WEP is applied. From 30 to 20 years, a sliding WEP scale is applied. Below 20 years, your benefit would drop even more. (For more information, click here.)

How does this affect your checks? The SSA offers this example: A person whose annual Social Security statement projects a $1,400 monthly benefit could get just $1,000, due to the WEP.

Your maximum loss is set at 50% of whatever you receive from your separate pension, so if that is relatively small, the WEP effect will be minimal.

You can still earn credits for delayed filing, and you will still get Social Security’s annual cost-of-living adjustment for inflation, but the WEP will still affect your initial benefit.

The WEP formula also affects spousal and dependent benefits during your lifetime. However, if your spouse receives a survivor benefit after your death, it is reset to the original amount.

Can you do anything to avoid getting whacked by WEP? Working longer in a Social Security-covered job before retiring might help. Remember, you are immune to the provision if you have 30 years of what Social Security defines as “substantial earnings” in covered work. That amounts to $22,050 for 2015.

So if you have 25 years, try to work another five, says Jim Blankenship, a financial planner who specializes in Social Security benefits. “That’s money in your pocket.”

Read next:The Pitfalls of Claiming Social Security in a Common-Law Marriage

Update: This story was updated to reflect that Social Security Administration gives little advance warning to beneficiaries, instead of no advance warning, and a description of Social Security benefits statements was added.

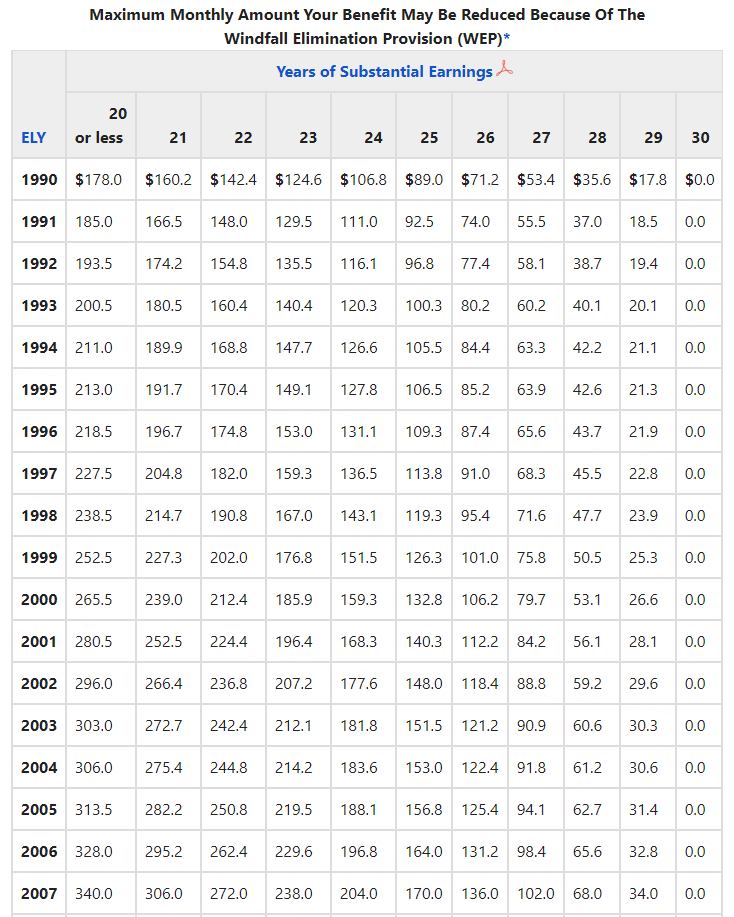

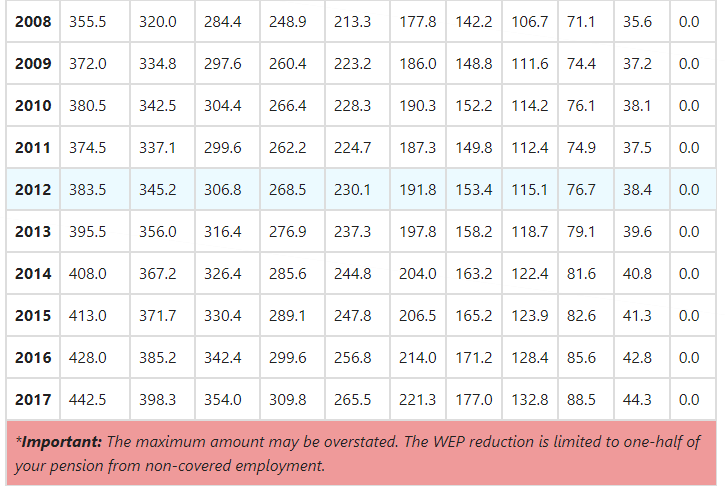

If you paid Social Security tax on 30 years of substantial earnings you are not affected by the Windfall Elimination Provision (WEP). … The following chart shows the maximum monthly amount your benefit can be reduced because of WEP if you have fewer than 30 years of substantial earnings.

Windfall Elimination Provision in Social Security

Note: You can find a table that lists the amount of substantial earnings for each year at the bottom of the second page of our Windfall Elimination Provision fact sheet.

The following chart shows the maximum monthly amount your benefit can be reduced because of WEP if you have fewer than 30 years of substantial earnings. (To calculate your WEP reduction, please use our WEP Online Calculator or download our Detailed Calculator.)

Important: The amounts in the chart do not reflect the effect of cost-of-living adjustments, early retirement, delayed retirement, or other factors.

Example: WEP reduces your Eligibility Year benefit before the annual cost-of-living adjustment (COLA) is added to your benefit. If you became disabled in 2008 (ELY 2008), presume the WEP reduced your $1,356 benefit to $1,000. In January, 2009 the 5.8% COLA increased your benefit by $58 ($1,000 x 5.8% = $58).

More examples of how other factors affect your retirement or disability benefits can be found in Examples: How the Windfall Elimination Provision Can Affect Your Social Security Benefit.

How To Use The Chart The chart is easy to use.

Go to the Eligibility Year (ELY) column to find the year you reach age 62 or became totally disabled (if earlier). If your birthday is on January 1st, use the year before you reach age 62.

Go to the column that shows the number of years you paid Social Security tax on substantial earnings.

The amount shown is the maximum your benefit can be reduced in your Eligibility Year because of the Windfall Elimination Provision (WEP).

Note: If your retirement benefits start after full retirement age or your non-covered pension starts later than your eligibility year, the WEP reduction may be greater than the maximum shown in the chart.

Continued–>

Windfall Elimination Provision – Social Security

How the Windfall Elimination Provision Can Affect Your Social Security …

If you are covered by a public sector pension, you may not get the Social Security payout you’re expecting.

Join my group on MeWe and see what is going on in the world.

.……Site was cancelled twice now……